This website contains the material related to CEMLA’s Growth at Risk Project (C-GARP). The C-GARP provides the first open-source platform for Growth at Risk analysis available to practitioners and researchers interested in using this methodology for analytical purposes.

The website is updated regularly with up-to-date outcomes of CEMLA’s Growth at Risk model and its related CEMLA Financial Conditions Index for a group of countries.

Please contact the C-GARP Office for any queries on the material at

.

.

The GaR concept was originally motivated as an extension of value-at-risk (VaR) models. While VaR models estimate expected investment losses conditional on market conditions, GaR models extend this idea to a macro level by estimating the expected distribution of GDP growth conditional on financial market conditions and other macroeconomic factors. For a detailed description of GaR models please go to C-GARP Documentation.

A GaR estimation includes the following main steps.

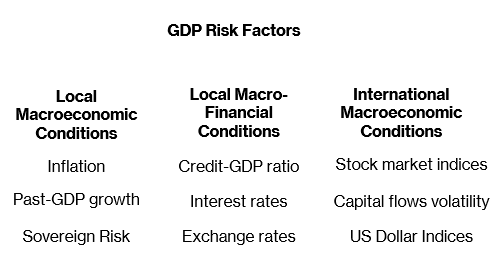

A first step is to identify variables that can arguably explain the dynamics in GDP growth, which represents the outcome variable in GaR models.

will have to make sure the prototype looks finished by inserting text or photo.make sure the prototype looks finished by.

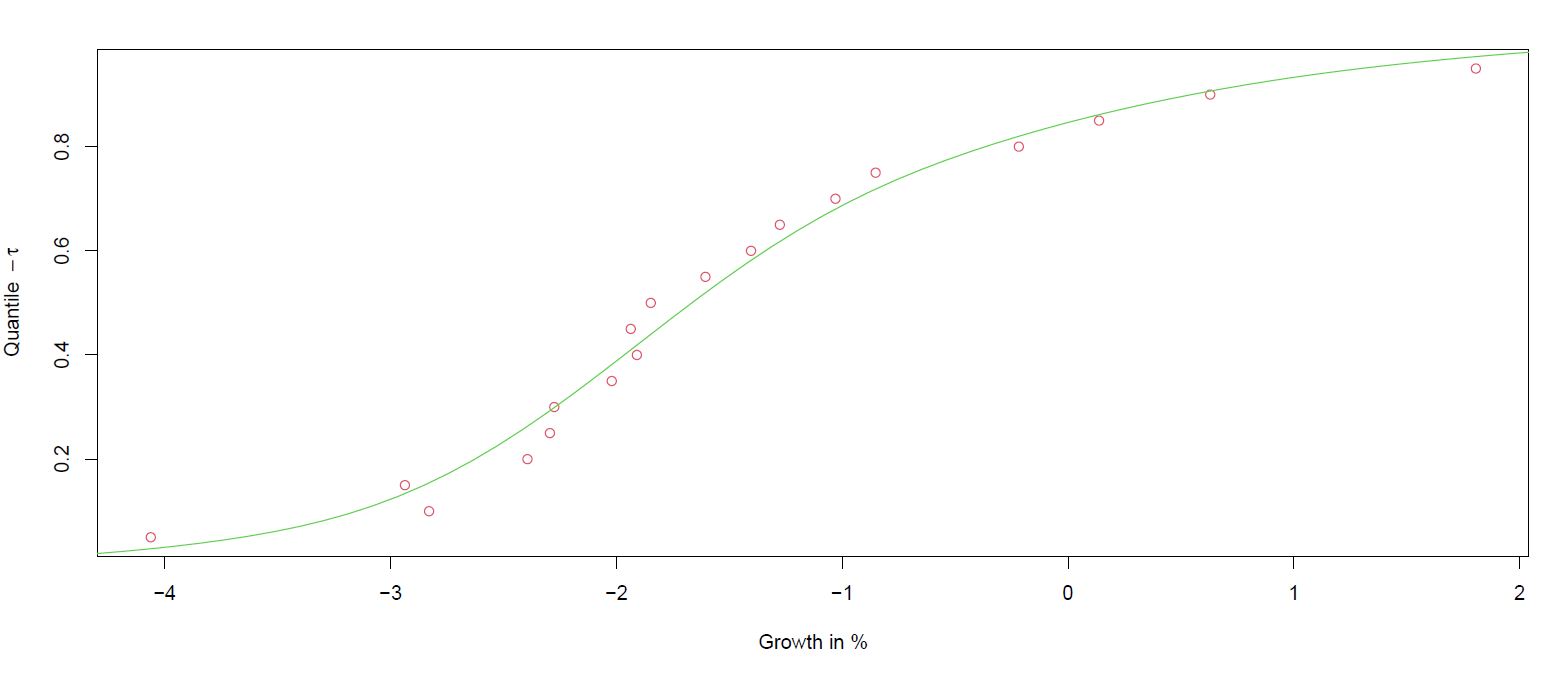

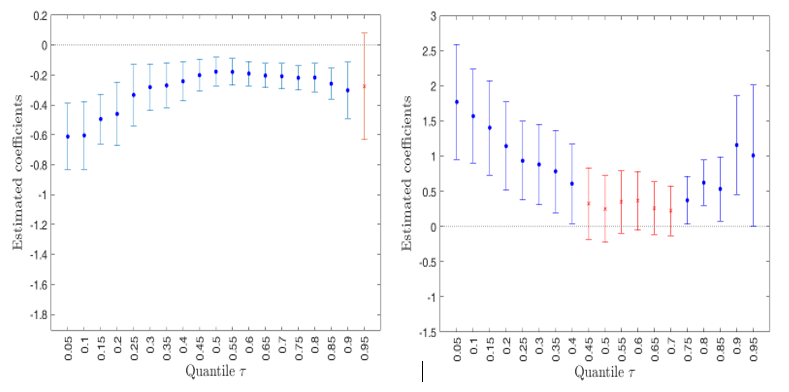

The point estimates from the quantile regressions (QR) can be interpreted as the values of the cumulative distribution function (CDF) of expected GDP growth.

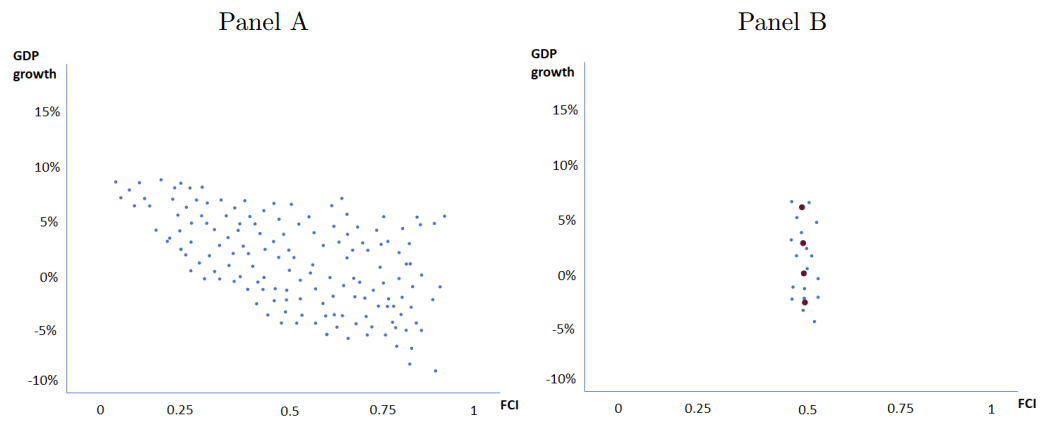

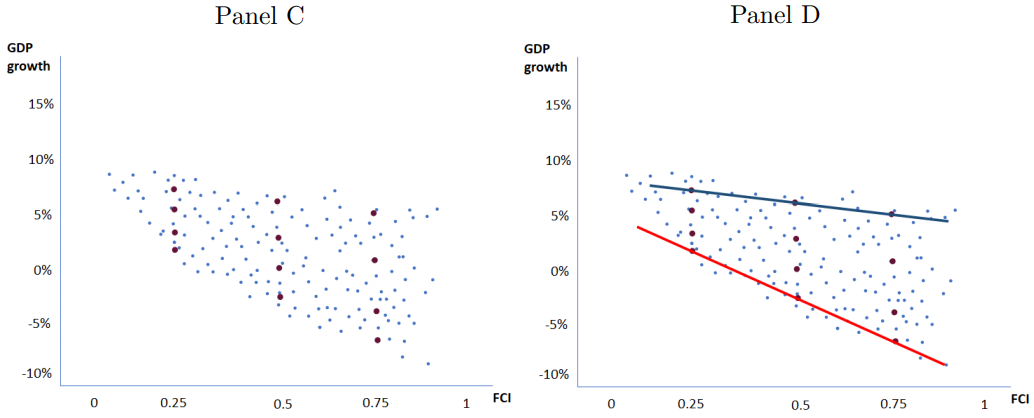

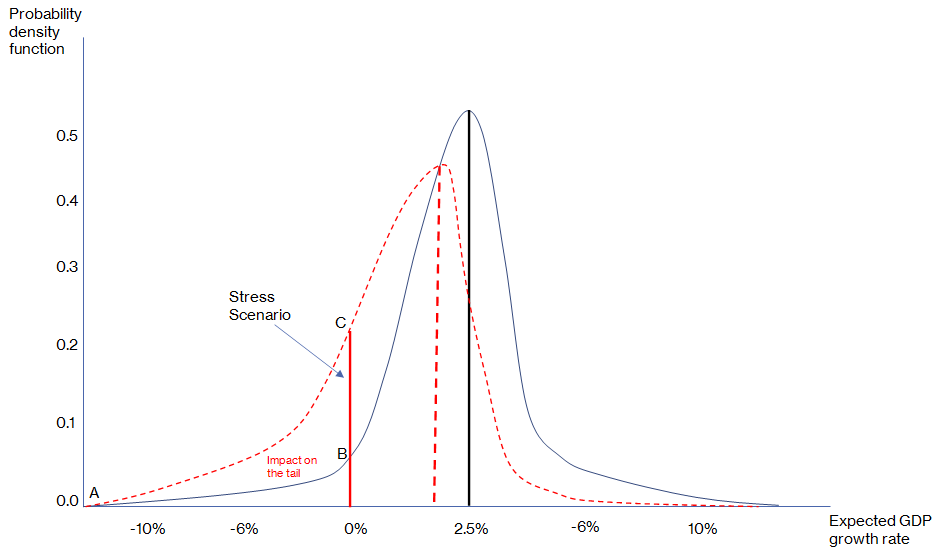

The main outcome of GaR estimations are expected GDP growth distributions conditional on the stance of macro-financial conditions.

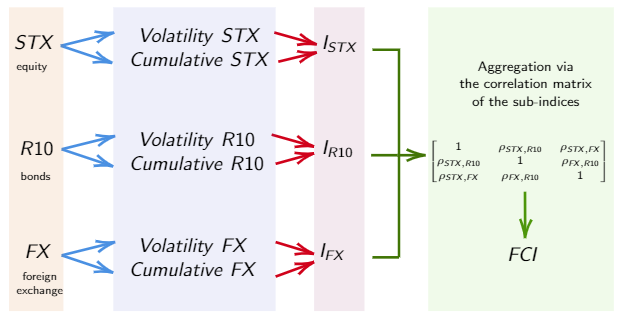

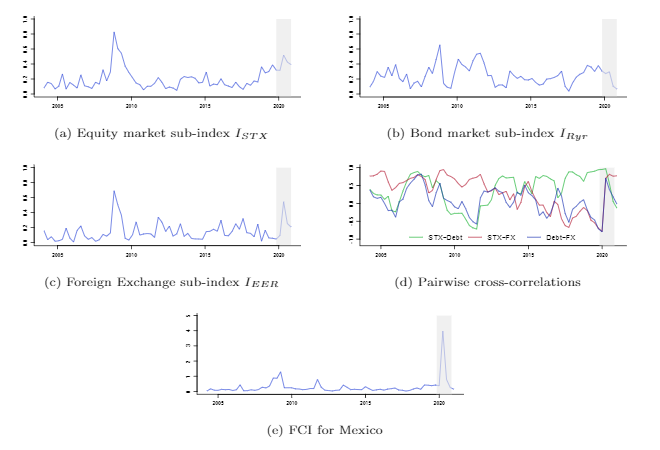

CEMLA Financial Conditions Index (FCI) represents a quarterly indicator of financial market stress computed for 5 Latin American economies: Brazil, Chile, Colombia, Mexico, and Peru. The index is constructed following the Country-Level Index of Financial Stress (CLIFS) methodology first proposed by Duprey et al. (2017). The index traces three buckets of financial stress indicators which are combined weighted by their bilateral historical correlations, adding a cross-sectoral spillover dimension to the index.

The FCI is constructed in the following way:

Note: End-of-quarter are estimates obtained from the underlying monthly index. The monthly series are available upon request.

CEMLA Growth-at-Risk estimations are reported as a combination of indicators showing variations over quarters in the probability of realizing a negative GDP growth scenario conditional on current macro-financial conditions. Results are drawn from a panel of five Latin American countries. We report the GaR estimations of quarterly estimated GDP growth conditional distributions.

This indicator reports the GDP growth rate that at least is expected to be realized if actual GDP growth falls within the 5th percentile of the estimated GDP growth distribution.

You can filter the countries using the labels with the names located at the bottom of the graph.

The GDP growth distribution for quarters from 2016Q1 onwards are estimated considering all the available data prior that date. For quarters before 2016Q1, the GDP growth distribution is obtained with the estimated model for 2016Q1 valuated on the data of the previous quarter.

Via the C-GARP project CEMLA makes available the material required to replicate and extend the CEMLA GaR model.

Technical Documentation: Please download the technical report that describes the steps followed for the construction of CEMLA’s Growth at Risk Model here.

Statistical programming code:

We provide access upon request to the programming code used for the construction of CEMLA’s Growth at Risk model. The code was written in R as its programming language in order to ensure its replicability in open-source statistical computing environments.

To request access to the code, send an e-mail at

.

including the following information:

The use of the code is restricted for the nonprofit use of CEMLA members and associates, central banks, financial regulators and academic institutions.

Below we provide the sources of the main variables of interest used to compute CEMLA Financial Conditions Index and to estimate CEMLA Growth-at-Risk Model.

For a detailed description of all methodological details and variables’ definitions please go to C-GARP Documentation.

Disclaimer

The data provided by the C-GARP Website is shown for informational purposes only. CEMLA does not bear any responsibility for its use and maintenance. The C-GARP Website provides several links to external websites as a convenience and for informational purposes only. These websites contain information created by other public, governmental, nonprofit and/or commercial organizations. The links to the websites do not constitute an endorsement by the C-GARP project of any of the data products, services, or opinions in the external websites. The C-GARP project bears no responsibility for the accuracy, legality, or content of the external links. Please contact the respective external site for questions regarding its content.

If you come across any external links that are not working, we would be grateful if you could report them us at

.

Email:

Web: www.cemla.org